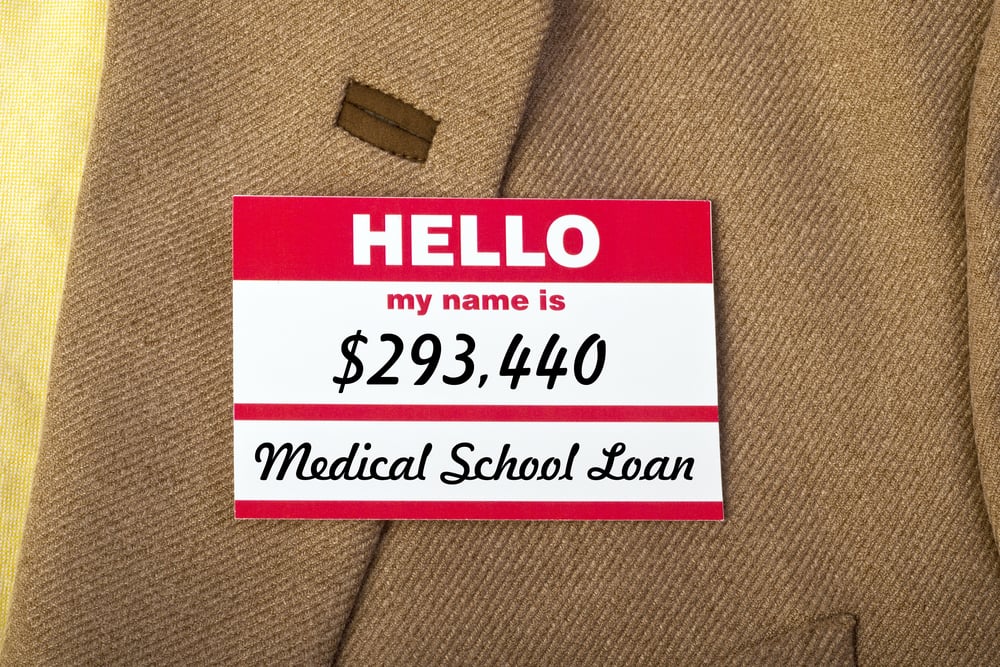

It is no secret that medical school is getting very expensive. Over the past 20 years, the cost of medical school has greatly outpaced the rate of inflation, and medical school debt is rapidly rising.

The average medical student now graduates with over $192,000 in student loans, but with the cost of attendance for the most expensive private medical schools approaching $100,000, there are some physicians who are finishing residency with $300,000 or even $400,000 in student loans.

The rate of increase in medical school tuition, with its increasing student loan burden as a consequence, has not significantly deterred college students from applying to medical school in record numbers. In 2017, 51,680 students applied for 21,338 spots.

While physicians have to take out massive amounts of student loan debt, because they enjoy the highest average salaries of any profession, student loans can typically be quickly paid off with only a few years of diligent saving.

However, are we reaching a point where it may no longer be financially prudent to attend medical school? For example, should a prospective primary care physician or pediatrician who might face up to half a million dollars in student loans consider against attending medical school?

Your patients are rating you online: How to respond. Manage your online reputation: A social media guide. Find out how.